Nearly five years ago, on September 15, Lehman Brothers Holdings Inc. filed for Chapter 11, the largest bankruptcy in the nation’s history. The move set off a series of dramatic actions in Washington, DC, and on Wall Street as bankers and regulators sought to avoid a shutdown of the global economy. To mark the anniversary, the Center for Public Integrity produced a three-part series on what has happened since the meltdown. This is Part One, focusing on the Wall Street bankers who fed the subprime mortgage machine, without regard to risk.

Five years after the near-collapse of the nation’s financial system, the economy continues a slow recovery marred by high unemployment, hesitant consumers and sluggish business investment.

Many of the top Wall Street bankers who were largely responsible for the disaster — and whose companies either collapsed or accepted billions in government bailouts — are also unemployed. But since they walked away from the disaster with millions, they’re juggling their ample free time between mansions and golf, skiing and tennis.

Meantime, the major banks that survived the crisis, largely because they were saved with taxpayer money after being deemed “too big to fail,” are now bigger and more powerful than ever.

The Center for Public Integrity looked at what happened to five former Wall Street kingpins to see what they are up to these days. None are in jail, nor are any criminal charges expected to be filed.

Certainly none are hurting for money.

Take Richard Fuld. Five years after Lehman Brothers Holdings Inc., the 158-year-old company he ran, collapsed under the weight of bad investments and sent a tidal wave of panic through the global financial system, Fuld is living comfortably.

He has a mansion in Greenwich, Conn., a 40-plus-acre ranch in Sun Valley, Idaho, as well as a five-bedroom home in Jupiter Island, Fla. He no longer has a place in Manhattan, since he sold his Park Avenue apartment in 2009 for $25.87 million.

The other four bankers the Center caught up with — Jimmy Cayne (Bear Stearns), Stanley O’Neal (Merrill Lynch), Chuck Prince (Citigroup) and Ken Lewis (Bank of America) are also living in quiet luxury.

Meltdown Primer

A quick crisis refresher: During the early years of the last decade, U.S. home values were soaring, fueled by ultra-low interest rates.

Wall Street investors, eager to get in on the party, developed an enormous appetite for bonds backed by the mortgages of everyday homeowners. Firms like Lehman would buy up thousands of mortgages, pool them together into a security, and sell the cash flow from the mortgage payments to investors, including pension funds and hedge funds.

The bonds were thought to be almost as safe as U.S. Treasuries, but they carried a higher interest rate.

The demand was so great that eventually mortgage lenders loosened their underwriting standards and made loans to people who couldn’t afford them, just to satisfy hungry investors.

When the housing market turned down in 2007 and homeowners began to default on their loans, the whole system began to crumble.

In March 2008, Bear Stearns almost collapsed and was sold. Six months later, Lehman failed, setting off a chain reaction that killed dozens more banks and mortgage lenders. Weeks later, Congress approved a $700 billion bailout of the financial system and soon nearly every major financial institution was on the dole.

The ensuing recession destroyed as much as $34 trillion in wealth and sent the unemployment rate soaring above 10 percent for the first time in 25 years.

“Every single one of these companies was insolvent,” said Neil Barofsky, the former special inspector general overseeing the bailout, which was called the Trouble Asset Relief Program.

“Clearly there was a large underpinning of fraud,” said Barofsky, a former federal prosecutor, who argues the government didn’t adequately pursue criminal charges against those who caused the crisis. “There was never really a comprehensive investigation. The Justice Department largely outsourced this to the Securities and Exchange Commission.”

Five years after the meltdown, the potential for a criminal prosecution of any of those involved in the events leading up to the collapse has faded as the statute of limitations for financial fraud ran out.

The five ultra-rich former Wall Street chieftains have simultaneously faded into luxurious obscurity while the survivors — Jamie Dimon of JPMorgan Chase & Co. and Lloyd Blankfein of Goldman Sachs — have only consolidated their power as they alternate between being seen as great villains or near statesmen depending on the changing fortunes of their companies.

Fuld Checks In

Five years after Lehman Brothers declared bankruptcy, Fuld is keeping a low profile. He’s not giving interviews or lectures, and he’s not done an apology tour.

At times he picks up the phone and calls up former Lehman co-workers — those whom he considers friends — to check in.

Kevin White, a former managing director at Lehman, says he hears from Fuld about once a month. The former CEO asks about White’s family, checks on how business is at the hedge fund White founded after Lehman, offers to help, and perhaps introduce him to someone.

“Dick’s a family man and he’s someone who takes this whole Lehman bankruptcy very personally,” White says. He admits that some of his former colleagues hate Fuld and don’t understand why White stays in touch.

Fuld has been widely criticized, by former Lehman workers and in official investigations, for allowing the firm to drown itself in too much debt. When it went bankrupt, for every dollar of capital Lehman held, it was borrowing at least $30. Some reports say the rate was higher than 40 to 1.

That gave it no cushion to absorb losses when the market began to decline.

The myriad investigations into the causes of the crisis revealed that under Fuld’s watch, Lehman executives toyed with the company’s finances to make that leverage look better than it really was using what some Lehman employees called an “accounting gimmick” called Repo 105, according to the official bankruptcy report by Anton Valukas of the law firm Jenner & Block.

The tactic allowed the company to characterize a short-term loan as an asset sale and then use the money from that false sale to cut debt. By doing so, Lehman appeared to have less debt and more cash. Lehman used Repo 105 transactions to cut the debt on its books by as much as $50 billion just before it announced quarterly earnings, giving investors a false impression of the bank’s financial health.

In a legal filing in an investor lawsuit, Fuld and other Lehman executives said investors were informed that Lehman’s leverage was often higher than it was at the end of each quarter.

"Lehman specifically disclosed that its balance sheet ‘will fluctuate from time to time’ and could be and at times was larger than its balance sheet reported at quarter- or year-end,’ the filing said.

Fuld, in testimony before the Financial Crisis Inquiry Commission, blamed Lehman’s failure on the government’s decision not to give it a bailout.

“Lehman was forced into bankruptcy not because it neglected to act responsibly or seek solutions to the crisis, but because of a decision, based on flawed information, not to provide Lehman with the support given to each of its competitors,” he testified.

“There is sufficient evidence … that Fuld was at least grossly negligent,” Valukas wrote in his report.

Negligence isn’t necessarily a crime, however, so Fuld has faced no punishment for the wreckage caused by his company’s collapse, save perhaps banishment to irrelevance.

Last year a federal judge approved a $90 million settlement of a class action suit brought by Lehman investors against Fuld and several other company executives and directors. The judge, Lewis Kaplan, questioned whether the settlement, which will be paid entirely by Lehman’s insurers, was fair given that none of the individuals would pay out of pocket. He agreed to the deal, however, because litigation expenses for a trial were likely to deplete the funds available for compensating the investors.

Fuld quietly opened his own advisory firm called Matrix Advisors in a Third Avenue office building in Manhattan, across the street from the headquarters of Avon, the cosmetics company. He’s landed a few clients, according to news reports, SEC filings and court records. Matrix advised AT&T Inc. on its failed bid to purchase T-Mobile. And it has consulted with GlyEco, a company that recycles the chemical glycol, and Ecologic Transportation Corp., a company that rents out environmentally friendly cars.

He was recently spotted at Doubles, the private dining club in the Sherry-Netherland Hotel in Manhattan, according to a former Lehman employee.

Still, companies haven’t been eager to have their names associated with Fuld, so landing clients hasn’t been easy, according to two people familiar with the business.

Fuld, through his lawyer, declined several interview requests for this story. He wasn’t in his office when a reporter paid a visit in July. His assistant, through a security guard, declined to say where he was.

Even if business is slow, it may not matter much to Fuld. Unlike many of his former employees, and unlike the millions of people still out of work after the 2008 financial collapse, Fuld has money.

When Lehman Brothers filed for bankruptcy on Sept. 15, there was a sense that if Fuld had mismanaged Lehman to death, at least he had lost a load of cash in the process as the value of his company stock dropped to nothing.

And he did lose plenty.

Fuld’s 10.8 million shares of the company that may have once been worth more than $900 million, according to a study by Harvard University Professor Lucian Bebchuk, became worthless.

However, he wasn’t exactly on his way to the poor house. From 2000 through 2007, Fuld took home as much as $529 million from his Lehman job. That includes his salary and cash bonuses, as well as the Lehman shares granted him by the company that he sold before the bankruptcy in September 2008.

That total comes from an analysis by Oliver Budde, a former Lehman associate general counsel who left the firm in 2006 because, he says, Lehman was underreporting its executive compensation to shareholders.

That income allowed Fuld to buy some very high-end real estate.

In Greenwich, he has an $8 million, nine-bedroom home with a guest house. He and his wife, Kathleen, bought the house in 2004 after they sold their previous Greenwich home to Robert Steel, a Goldman Sachs executive who became undersecretary of the Treasury in 2006 under Henry Paulson. Steel then became CEO of Wachovia, which nearly collapsed 11 days after Lehman and was sold to Wells Fargo at the direction of federal regulators.

When he’s looking to get out of Greenwich, Fuld can head south to Jupiter Island, Fla., a ritzy barrier island that’s home to Tiger Woods and Greg Norman. He transferred ownership of the $10.6 million beachfront home, with a pool and tennis court, to his wife in November 2008, a common strategy for protecting assets from legal judgments.

He also spends a lot of time at his 40-plus-acre ranch in Ketchum, Idaho, in the center of the Sun Valley resort area. The spot offers “ultimate privacy,” according to Daryl Fauth, CEO of Blaine County Title in Ketchum.

The ranch is located just five minutes from downtown Ketchum, east of the Baldy Mountain ski resort and west of the Reinheimer Ranch, a 110-acre spread that’s owned by the Idaho Foundation for Parks and Lands and can’t be developed. The house is situated on a bend in a river that runs through the property.

Fuld even managed to make a killing in real estate during the depths of the collapse. A Park Avenue apartment that he and his wife bought in 2007 for $21 million was sold in 2009 for a $4.8 million gross profit.

What he hasn’t done is make any public statement or gesture or obvious effort to rehabilitate his image. He hasn’t made any public overtures to major charities.

He appears to have wound down his family foundation after Lehman went bankrupt, distributing the last $10,948 in 2009, according to tax filings. And last summer Fuld sued his estranged son-in-law seeking to recover money he had lent the younger man to buy a home with Fuld’s daughter.

Fuld was looking to be paid in cash and stock by those he advised, according to a person familiar with the company. That’s the type of agreement he struck with Ecologic, which paid him a $10,000-per-month retainer and granted him options to buy 2.29 million shares of its stock at 25 cents per share.

Jimmy’s Playing Bridge

While Fuld has tried to stay in the business, Jimmy Cayne of Bear Stearns has withdrawn completely.

Cayne, who lives in a $25 million apartment in New York’s Plaza Hotel, can be found almost every day in cyberspace hosting an online bridge game.

Last month in the Hyatt Regency hotel in Atlanta, Cayne sat for hours in a crowded ballroom with orange, brown and yellow swirled carpet competing for the coveted Spingold Cup.

Cayne sat in a crisply pressed shirt with his team — two Italians and two Israelis — chomping a cigar and talking in hushed tones over one of the dozens of folding tables. He likely pays his players more than $100,000 a year each to help him remain atop the world rankings, according to two people who have played in tournaments against him.

He’s ranked 22nd in the world, according to the American Contract Bridge League. Last month he lost in the round of 16 of the Spingold knockout match.

That he’s opted for bridge over finance is telling, as Cayne was much criticized for spending more time on golf and bridge than on dealing with the crises that were crushing his firm.

While at Bear, Cayne would leave every Thursday and take a helicopter to his New Jersey beach house for long weekends of golf at the Hollywood Golf Club. He’d emerge from the chopper behind sunglasses and chomping the trademark cigar, according to people who saw him there.

Cayne had survived the bankruptcy of two Bear Stearns hedge funds the summer before but succumbed to the inevitable when, in the fourth quarter of 2007, the company had to write down $1. 9 billion in bad home loan bets, leading to its first quarterly loss ever.

He retired as CEO in January 2008, two months before the firm collapsed under the weight of its subprime mortgage investments, but remained as board chairman. As the market became doubtful that the mortgage bonds on Bear’s books were worth what the company claimed, companies pulled their business, suddenly and en masse.

Bear Stearns was sold on March 16, 2008, in a late night deal to JPMorgan Chase & Co., which eventually paid $1.2 billion, about what it would have cost to buy the company’s Madison Avenue headquarters.

The company’s leverage ratio was 38 to 1 or higher, according to Phil Angelides, the chairman of the Financial Crisis Inquiry Commission. Cayne acknowledged in his testimony before the commission that it was too high.

“That was the business,” he said. “That was really industry practice.”

He told Angelides that he believed in Bear so strongly that he almost never sold its stock. “I rarely sold any of the firm’s stock except as needed to pay taxes,” he testified on May 5, 2010.

Like Fuld, Cayne lost about $900 million on paper when Bear’s stock plunged, but he took home plenty before the crash. He earned $87.5 million in cash bonuses from 2000 to 2007 and sold stock worth about $289.1 million in those years, according to Bebchuk’s study.

In addition to the Plaza Hotel condo, he and his wife have a second apartment on Park Avenue. They put that home on the market last month for $14.95 million. When they want to get out of the city, they can head to their $8.2 million mansion on the Jersey Shore, about a mile from the Hollywood Golf Club, or their $2.75 million condo at the Boca Beach Club in Boca Raton, Fla.

Cayne, like many of his fellow CEOs, has apparently worked to shield his assets from potential liability.

In November and December 2009, he transferred ownership of four pieces of real estate to four separate limited liability companies, called Legion Holdings I, II, III and IV, for a total of $21. Some of the LLCs share Cayne’s Plaza Hotel mailing address in public tax records.

“I take responsibility for what happened. I’m not going to walk away from the responsibility,” Cayne told the FCIC.

He hasn’t had to take any for the demise of Bear, however. He’s paid no judgments or settlements from any lawsuits, according to his lawyer, David Frankel.

Chuck Prince is Helping his Friends

While Fuld went down with his ship and Cayne remained until close to the end, two of their CEO brethren were pushed aside earlier — when the subprime collapse began taking its toll on profits — only to watch their companies falter from a distance.

Charles O. Prince III resigned as CEO of Citigroup on Nov. 5, 2007, when the company announced it had lost between $8 billion and $11 billion on subprime mortgage bets.

“Given the size of the recent losses in our mortgage-backed securities business, the only honorable course for me to take as Chief Executive Officer is to step down,” he said in a statement. Prince walked away with a golden parachute worth about $33.6 million.

From 2000 through his resignation, Prince took home $65.2 million in cash salary and bonuses, according to an analysis by the Center. There are no SEC reports showing that he sold any shares from 2000 through 2008. It’s unclear whether he’s sold any since he resigned. Citigroup shares were priced at more than $300 the week Prince resigned and today hover at about $50 after a 1-for-10 reverse stock split.

His downfall came only months after he famously justified Citi’s continued involvement in subprime:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing,” he told The Financial Times in July 2007.

Prince was succeeded by Vikram Pandit, a former hedge fund manager whose firm was acquired by Citi just months earlier for $800 million. While Pandit was trying to right the listing ship, the company continued to provide Prince with an office, an administrative assistant and a car and driver for up to five years, a package worth $1.5 million a year, according to SEC filings.

By the end of 2008, Citigroup had received $45 billion in bailout money from the U.S. Treasury and the Federal Reserve had guaranteed hundreds of millions of dollars of its debt.

Prince apologized for the disaster that the financial crisis caused in testimony to the FCIC in 2010. "I'm sorry the financial crisis has had such a devastating impact for our country," he testified. "I'm sorry about the millions of people, average Americans, who lost their homes. And I'm sorry that our management team, starting with me, like so many others, could not see the unprecedented market collapse that lay before us."

After Citigroup, Prince joined the global consulting firm Stonebridge International, which was founded by former National Security Advisor Sandy Berger. The company merged in 2009 with the Albright Group, founded by former Secretary of State Madeleine Albright to form Albright Stonebridge Group.

Prince described his move to Albright Stonebridge as “helping my friends with their activities,” in a 2009 interview. When pressed about what his exact job was he said, “I’m just a friend.”

He’s no longer listed as an executive on the company’s website and a spokeswoman for the company did not respond to an email and phone call seeking an update on his status.

He serves on the boards of directors of Xerox Corp. and Johnson & Johnson Inc. He’s represented by the Harry Walker Agency as a speaker for hire on topics including “Corporate Governance: A Five-Point Plan to the Best Business Practices,” and “Inside the Current Financial Crisis.”

Last year Prince, along with Citigroup and several members of the company’s pre-2008 board, settled a class action lawsuit for $590 million that accused them of misleading investors about the amount of subprime-related securities the company held on its books and underreporting losses related to those investments. Prince and the other defendants didn’t admit any wrongdoing in the settlement.

It’s unclear how often Prince went to the office held for him at Citi, but what is clear is that Prince had plenty of other places to spend his time.

He has a $3.6 million Nantucket getaway and a $2.7 million house in a Jack Nicklaus golf community in North Palm Beach, Fla., called Lost Tree Village.

Stan O’Neal Goes to the Vineyard

Prince’s ouster from Citigroup was prefaced just days earlier by the departure of Stanley O’Neal from Merrill Lynch.

O’Neal had taken over Merrill when it was mostly a retail brokerage firm and turned it into a major manufacturer of collateralized debt obligations, a type of security, backed by home mortgages.

By 2006, it was the biggest underwriter of CDOs on Wall Street and a year later the company had $55 billion worth of subprime loans on its own books that no one wanted to buy.

As the losses mounted, O’Neal made overtures, first to Bank of America, then to Wachovia, about buying Merrill Lynch — without the approval of the board, according to a 2010 interview O’Neal gave to Fortune Magazine. When in October 2007 Merrill announced it was writing off $8 billion of its mortgage-backed securities, and then news broke that O’Neal was thinking of selling the firm, it was over. He was fired.

O’Neal floated out of Merrill comfortably, however, buoyed by a golden parachute worth $161.5 million. In the eight years leading up to his ouster, O’Neal earned $68.4 million in cash salary and bonuses, and he sold Merrill stock at a profit of at least $18.7 million, according to a Center review of annual reports and SEC filings.

He was succeeded by John Thain, a former CEO of the New York Stock Exchange, who convinced Bank of America to buy Merrill Lynch for $50 billion just as Lehman was imploding and taking much of the financial system with it.

(Thain himself was eventually fired after it became public that he spent more than $1 million renovating his Merrill office — including $87,700 for a pair of guest chairs — as the company was on the verge of bankruptcy.)

O’Neal, however, is flush. On top of his $161.5 million, he and his wife have a Park Avenue apartment. NBC anchor Tom Brokaw sold his apartment in the building for $10.75 million in 2011. O’Neal transferred full ownership to his wife in November 2008, a common strategy to protect the home from any legal judgments.

The couple also owns a $12.4 million vacation home in Martha’s Vineyard through an LLC called KZ Vineyard Land.

Today he sits on the board of Alcoa Inc., the world’s top producer of aluminum and is on the audit and corporate governance committees.

Ken Lewis Moves to Florida

Kenneth Lewis survived the September 2008 bloodbath and even came out looking like a hero to some when he arranged Bank of America’s hasty purchase of Merrill Lynch — O’Neal’s former employer — for $50 billion on the same weekend that Lehman failed, possibly saving it from the same fate as Lehman.

It soon became clear that Merrill was no bargain. That, combined with Lewis’ ill-advised purchase of subprime giant Countrywide Financial just as the housing market went into free fall, led Bank of America to start hemorrhaging cash.

It eventually got $45 billion in bailout money from the federal government to stanch the bleeding.

Lewis knew of Merrill’s excess losses before shareholders approved the final deal, according to his 2009 testimony to then-New York Attorney General Andrew Cuomo. He said he kept the losses hidden under pressure from Treasury Secretary Henry Paulson who worried that, if the deal fell through, it would hurt the already wounded market and overall economy.

Bank of America last month was accused by the Justice Department in a civil lawsuit of understating the risks that the loans included in $850 million of mortgage-backed securities would default. The Justice Department said the company was so hungry for loans to securitize that it let its quality controls slide and didn’t adequately verify borrowers’ incomes or ability to repay. The suit did not name Lewis as a defendant.

The company already settled a civil fraud suit with the SEC for $150 million and another lawsuit brought by pension fund investors for $62.5 million.

Lewis retired in September 2009 with a going-away package worth $83 million, even though the company was largely dependent on the federal government for its survival. He had already banked at least $86.4 million from Bank of America stock sales between 2000 and 2008, according to SEC filings. He also brought in $52.4 million in salary and bonuses in that time.

He and his wife Donna sold their house in Charlotte, N.C., in January for $3.15 million and their mountainside mansion in Aspen for $13.5 million, $3.35 million less than what they paid for it in 2006.

They appear now to have only one home, a $4.1 million condo in a beachfront high-rise in Naples, Fla.

The Winners

While Lewis and several of the CEOs that led their companies into the thicket of mortgage-backed securities have ended up rich but unemployed, two have seen their fortunes soar.

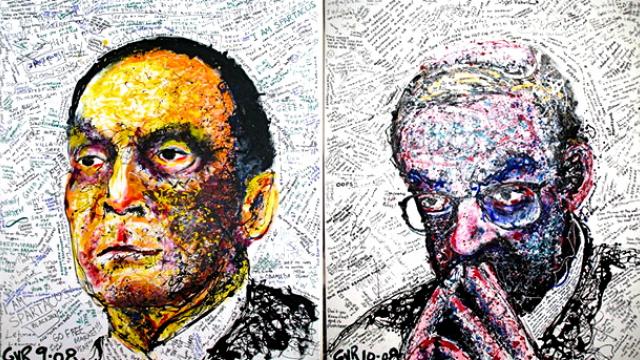

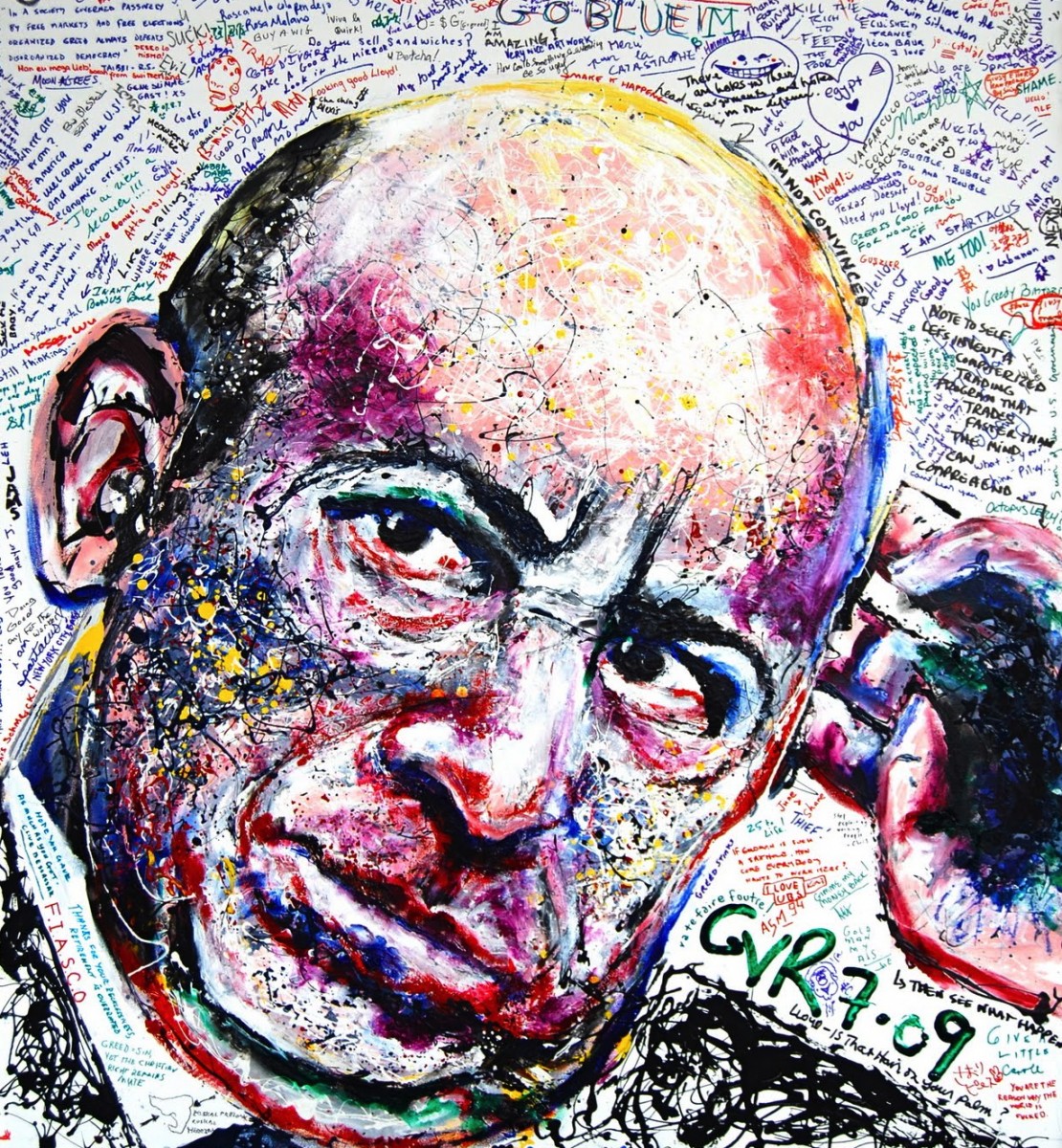

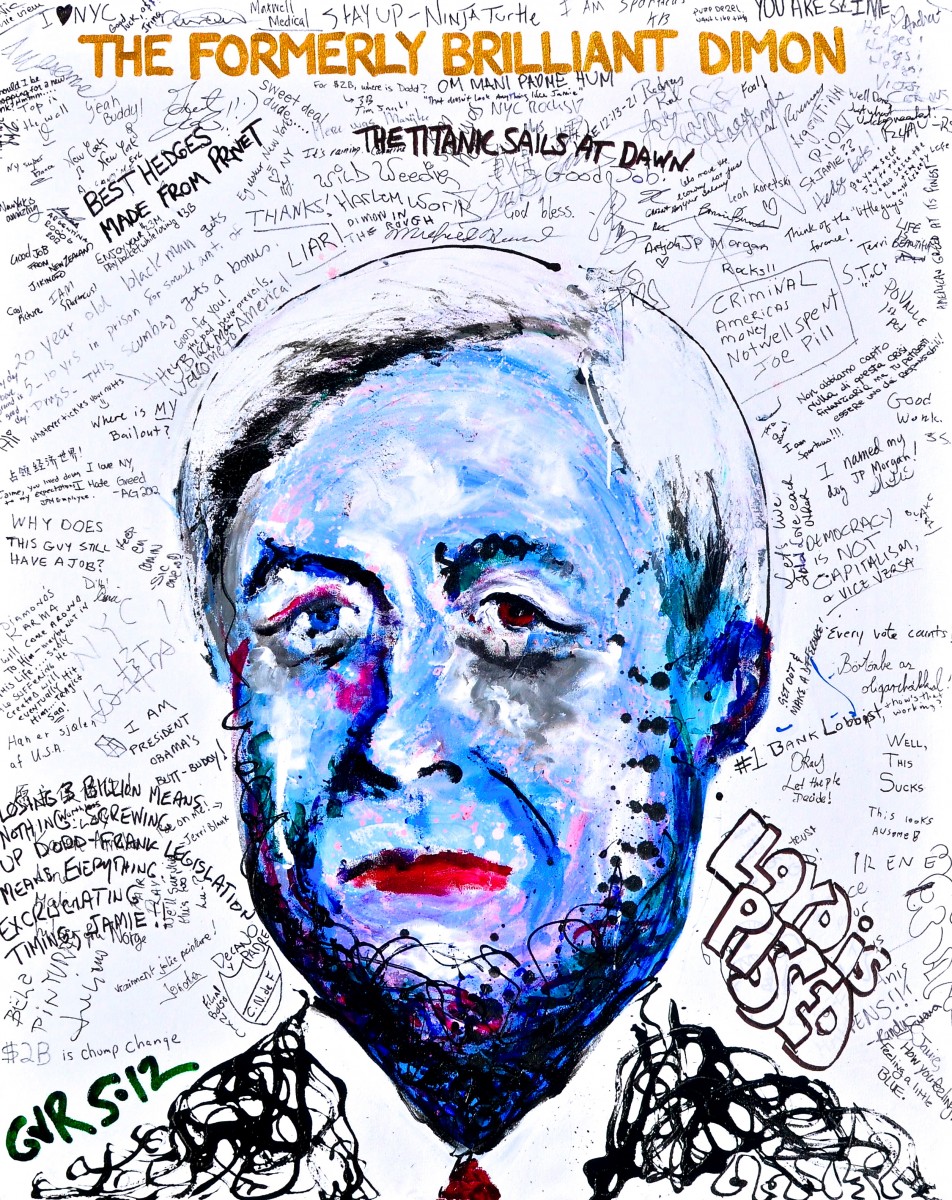

Jamie Dimon and Lloyd Blankfein, the leaders of JPMorgan Chase & Co. and Goldman Sachs Group Inc., today stand atop the global financial system, their banks bigger and more powerful than ever and their personal fortunes growing.

Blankfein was a magnet for scorn and envy before the crisis when Goldman awarded him a $68 million bonus in 2007, just as the economy was going bad. He then became the target for much of the public wrath that followed the collapse of the economy when he flippantly declared that Goldman was doing “God’s work” by lending money to businesses.

His reputation plummeted to its lowest point in 2010 after revelations that Goldman Sachs packaged and sold mortgage securities that appeared designed to fail, and then shorted the bonds, making a killing for the firm while customers lost money.

The company was sued by the SEC over one such deal, called Abacus, and Goldman settled the case for $550 million without admitting any wrongdoing.

While Blankfein was the villain, Dimon was treated as a rock-star statesman.

He was welcome at the White House and lauded as one of the only bankers who didn’t need a bailout — even though he took one, allegedly at the direction of Paulson.

Obama sang his praises in February 2009, just weeks after entering the Oval Office.

“There are a lot of banks that are actually pretty well managed, JPMorgan being a good example,” Obama said. “Jamie Dimon, the CEO there, I don't think should be punished for doing a pretty good job managing an enormous portfolio.”

Dimon’s popularity in the White House began to fade because he was a vocal opponent of many of the financial reforms being advocated in response to the crisis. Then in 2012, JPMorgan announced it had lost billions because of bad bets by a rogue derivatives trader in London.

Dimon came under investigation for minimizing the issue to investors — he called the problem “a tempest in a teapot.” The company was sued by the SEC, and Dimon had to testify before Congress. Last spring he barely survived a shareholder vote that would have separated his two jobs, chairman of the board and chief executive.

Last month the company said it was under civil and criminal investigation by the Justice Department over its subprime mortgage-backed securities.

When he hit the nadir of his troubles, Dimon reportedly sought advice from Blankfein on how to weather the storm and maintain his and his company’s reputation.

Earlier this summer, Blankfein held forth before a roomful of journalists and lobbyists at Washington’s swank Mayflower Hotel where, like an elder statesman, he was asked about everything from immigration reform to his first job selling hot dogs at Yankee Stadium. BusinessWeek Magazine wrote a story about the fashion impact of his new beard.

Through the ups and downs, neither CEO has suffered financially.

Blankfein was paid $21 million last year and he was the highest-paid chief executive of the 20 biggest financial companies, according to Bloomberg. Dimon earned about half that, or $11.5 million, as a result of the derivatives loss that became known as the “London whale.” Blankfein owns about $256 million of Goldman shares, according to Forbes magazine.

Dimon bought a Park Avenue apartment in 2004 for $4.9 million and bought a second unit in the same building this year for $2 million. He also owns a $17 million estate in Mt. Kisko, N.Y. Blankfein’s Central Park West penthouse is valued at $26.5 million, according to New York property records. Late last year, he and his wife also bought a 7.5-acre estate in the Hamptons with a pool and tennis court for $32.5 million. Forbes estimates Dimon owns $223 million of JPMorgan stock.

While Dimon and Blankfein held on to their power, the banks they lead, and other U.S. megabanks, have grown larger and more powerful.

JPMorgan’s assets — one common measure of bank size — have grown to $2.44 trillion from $1.78 trillion shortly before Lehman failed in 2008. Bank of America’s assets have ballooned to $2.13 trillion from $1.72 trillion, while Wells Fargo more than doubled to $1.44 trillion from $609 billion five years ago. Goldman Sachs, which wasn’t on the list of top 50 bank holding companies in 2008 because it was a pure investment bank at the time, is now the nation’s fifth largest with $939 billion in assets.

Citigroup, beset by financial problems, is the only one of the top five banks whose balance sheet has shrunk in those years.

Total assets don’t even adequately measure the full size of these institutions because the measure does not take into account derivatives contracts or off-balance-sheet items that could still put the banks at risk. If those assets were counted, JPMorgan’s size would rise to $3.95 trillion, according to a worksheet prepared by FDIC Vice Chairman Thomas Hoenig.

‘Bad Guys Everywhere’

Since that epic month in 2008 that began with the bankruptcy of Lehman early Monday, Sept. 15, and ended with the $80 billion bailout of insurance giant American International Group and the sales of Merrill Lynch to Bank of America, Wachovia to Wells Fargo and Washington Mutual to JPMorgan, thousands of hours and millions of pages have been filled trying to determine what happened.

The most comprehensive, the Financial Crisis Inquiry Report, said the financial collapse was avoidable.

“The captains of finance and the public stewards of our financial system ignored warnings and failed to question, understand, and manage evolving risks within a system essential to the well-being of the American public. Theirs was a big miss, not a stumble,” the report said.

That those “captains of finance” have suffered few consequences of that “big miss” is now part of the legacy of the crisis, and has cast a shadow over the U.S. justice system, which prosecutes small-time offenders but appears to turn away from what many see as crimes of the wealthy.

“This is the greatest white-collar fraud and most destructive white-collar fraud in history and we have found ourselves unable to prosecute any elite bankers,” said Bill Black, an economics and law professor at the University of Missouri and author of The Best Way to Rob a Bank is to Own One. “That’s outrageous.”

U.S. Attorney General Eric Holder appeared to confirm that view earlier this year when he said he’s hesitant to criminally prosecute big banks because he’s afraid of the damage such a move could do to the economy.

“When we are hit with indications that if you do prosecute, if you do bring a criminal charge, it will have a negative impact on the national economy, perhaps even the world economy … that is a function of the fact that some of these institutions have become too large,” he said during a Senate Judiciary Committee hearing in March.

Since that time, the Justice Department has walked back those statements and assured lawmakers and the public that they have aggressively investigated and pursued any criminal acts related to the financial crisis.

The hurdle, officials say, is that to prove a crime, they must prove intent. That means if the government wanted to bring charges against any of the CEOs of the companies that led the nation to financial disaster, prosecutors would have to prove to a jury beyond a reasonable doubt that these individuals intended to commit fraud.

“They tend to have to work in a much more black and white misconduct universe,” said Jordan Thomas, a former lawyer for the SEC who worked with Justice on many financial fraud cases. Proving criminal misconduct is such a high hurdle that the government has resorted mostly to civil charges, where the burden of proof is lower. That doesn’t mean, Thomas says, that nobody did anything wrong.

“The financial crisis had bad guys everywhere,” he said.

Ben Wieder contributed to this report.

3 WAYS TO SHOW YOUR SUPPORT

- Log in to post comments